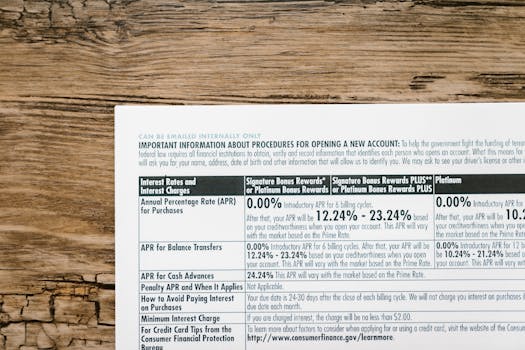

Staring at your bank statement and seeing unexpected fees is a universal annoyance. Every year, millions of account holders discover that their well-intentioned banking habits can end up costing extra.

Understanding bank fees isn’t just about the dollars and cents you lose. It’s also about feeling in control of your money, avoiding frustration, and keeping more cash in your pocket for the things that matter.

If you want to feel more empowered about your finances, keep reading. This guide breaks down major bank fees, why they sneak up on us, and, most importantly, what you can do to sidestep them.

Knowing Where Hidden Charges Lurk

When it comes to spotting bank fees, awareness is half the battle. Banks often tuck charges into the fine print, and it’s easy to miss what triggers each fee if you’re not looking closely.

Imagine your bank account like a road trip. If you don’t pay close attention to the directions, you can end up on bumpy roads or pay unnecessary tolls because you missed a sign.

- Monthly maintenance fees can appear if minimum balance requirements are not met. Review your account’s terms to know what triggers this recurring charge.

- Overdraft fees apply when you spend more than you have. These can happen even for small amounts, and repeated occurrences can snowball quickly.

- ATM fees occur when withdrawing cash from an out-of-network machine. Charges may come from both your bank and the ATM owner.

- Excess transaction fees are often applied to savings accounts that exceed a certain number of withdrawals each month.

- Paper statement fees are now common as banks encourage digital banking. Opting out typically saves a few dollars each month.

Each category exists for a reason, but keeping an eye out for these common culprits lets you navigate bank expenses like a seasoned traveler chooses toll-free routes.

Examining the Story Behind Minimum Balance Charges

A friend once realized she paid $12 each month for not keeping $1,500 in her checking account. Had she moved her savings to cover the gap, she could’ve avoided the fee altogether.

Another example: Someone with multiple small accounts found that by consolidating funds into just one, they were able to consistently meet the minimum balance, thus sidestepping charges entirely.

Sometimes, students or young professionals open accounts with high minimums, thinking they’ll be able to maintain them. It’s easy to misjudge cash flow, which later leads to these avoidable costs.

Checking your account choices regularly is smart. If a minimum seems out of reach, switching to a no-minimum account can save money and stress in the long run.

Breaking Down Bank Fee Types and Their Avoidance Techniques

Understanding each fee, and knowing your options, empowers you to make better choices. Here’s a closer look at the common types of banking fees, with strategies to avoid them.

- Monthly maintenance fees: Opt for accounts with no monthly fees or meet qualifying requirements, such as direct deposit or e-statements. Compare account types at your bank, as conditions vary.

- Overdraft fees: Sign up for overdraft protection, link to a savings account, or set account alerts. Overdraft fees add up fast, so prevention strategies often pay for themselves.

- Foreign transaction fees: Some banks waive these fees on certain checking accounts. Others have international branches or partners that minimize charges. Compare before traveling abroad.

- ATM fees: Stick to your bank’s ATMs. Mobile banking apps usually show fee-free locations, saving you from double charges—one from your bank, and one from the ATM owner.

- Paper statement fees: Switch to electronic statements. Most banks offer these for free, so it’s an easy fix that also streamlines your record-keeping.

- Excess transaction fees: Know the transaction limits on your savings account. Arrange transfers and withdrawals carefully, especially if you dip into savings frequently.

- Account closure fees: Stay aware of minimum open periods. Closing an account too soon sometimes triggers a penalty. Read the terms, and plan your account changes accordingly.

By knowing which fees apply and the best way to avoid each, you greatly reduce unnecessary expenses and keep your financial routine running smoothly.

Comparing Banks: Not All Account Features Are Created Equal

Some folks stick with their childhood bank out of habit, while others treat banking like shopping for shoes—comfort and features matter most. The choice can have a big effect on your bottom line.

For instance, one bank may offer free checking with no minimum balance, while another charges a fee unless you jump through specific hoops. Like picking between fast food or a nice sit-down meal, each fits different preferences and budgets.

| Account Type | Monthly Fee | Minimum Balance |

|---|---|---|

| Standard Checking | $10 | $1,500 |

| No-Fee Checking | $0 | $0 |

| Online-Only Account | $0 | $0 |

Reviewing options as shown in the table can help you select an account that fits your lifestyle, avoids hidden costs, and supports your savings over time.

Tactics for Navigating ATM Surcharges and Network Fees

ATM surcharges often seem inevitable, but they’re not. Think of using an out-of-network ATM like stopping for overpriced snacks at a highway rest stop—it’s convenient but bites into your cash.

Say you use a non-affiliated ATM and pay $3 from your bank and $3 from the ATM operator each time; that’s $6 per withdrawal, which quickly multiplies. Planning withdrawals ahead can help dodge this trap.

Online banks and credit unions frequently waive ATM fees or reimburse customers monthly up to a limit. Switching to one of these might seem like changing neighborhoods to avoid getting towed—a little hassle upfront, but you’ll avoid regular fines.

You can also use cash back at the register instead of standalone ATMs. Just like grabbing milk while picking up groceries, bundling financial activities saves you time, money, and unnecessary fees.

Smart Habits to Keep More of Your Cash

- Set balance alerts to avoid accidental overdrafts or falling below minimum thresholds.

- Use your bank’s mobile app to monitor activity and spot fees promptly.

- Automate transfers to savings accounts for penalty-free, scheduled growth.

- Choose e-statements to dodge paper statement fees and organize your records digitally.

- Schedule bill payments to avoid late fees and keep your account in good standing.

- Review account terms annually to catch policy changes that might introduce new fees.

- Consider switching banks if your needs or banking habits shift over time.

Every small action stacks up, like regularly changing your car’s oil to prevent expensive engine problems. These habits help you dodge fees while keeping your accounts healthy, no matter how busy life gets.

Reviewing your patterns at least once a year makes it easier to spot areas where you’re leaking money. That way, you can fix habits before they start costing too much.

Weighing Fee-Free Accounts Versus Paid Feature Accounts

Fee-free accounts may seem ideal at first glance, but sometimes paid accounts offer perks worth the extra cost—like airline mile rewards, premium customer service, or higher ATM withdrawal limits.

Choosing the right account is like selecting between public transportation and ride-sharing services. Both get you to your destination, but each suits different needs, schedules, and budgets. Some folks are willing to pay for an upgraded experience.

Consider what features matter most: Do you want flexibility, convenience, or rewards? Asking yourself what you’d do if fees were suddenly doubled can help clarify which account serves your lifestyle without financial stress.

Putting It All Together for Fee-Free Banking

Avoiding bank fees is a series of small, smart choices. The more you understand what, when, and why fees occur, the easier it is to navigate the banking world confidently and proactively.

Comparing account features regularly and building fee-avoidance habits keeps your finances healthier and more predictable. This lets you save for your goals without annoying setbacks or unpleasant surprises.

Banking doesn’t need to be complicated or expensive. A bit of attention and planning helps ensure most or all of your money stays with you, instead of getting chipped away by unnecessary fees.

Stay vigilant with periodic account reviews, embrace useful banking tools, and seek out accounts that match your needs. Your peace of mind and your budget will thank you for the effort.

Let this guide serve as your handy road map as you choose smarter banking options—so you can focus on what financial freedom truly means to you.